Every Friday, we feature mortgage programs, financing solutions, and guideline enhancements from our nationwide lending network. Explore the latest opportunities and discover financing options for homebuyers, homeowners, investors, and Realtors®

Once you think through your goals and determine how much home your

budget can handle, it’s time to choose a mortgage. With so many

different mortgages available, choosing one may seem overwhelming.

The good news is that when you work with Tag Lending Group,

our AI Mortgage Solution System will walk you through every step of the way!

Mortgage Intelligence

What are Loan Options?

Once you think through your goals and determine how much home your budget can handle, it’s time to choose a mortgage. With so many different mortgages available, choosing one may seem overwhelming. The good news is that when you work with Tag Lending Group. Our AI Mortgage Solution System will walk you through every step of the way!

LOAN PROGRAMS

Find the Right Mortgage Program with Confidence

Whether you're buying a home, refinancing, investing, or helping a client navigate financing, our Loan Programs platform makes it easy to explore mortgage solutions available through our nationwide network of over 100 lending partners.

Non-QM

Self-Employed

Bank Statements (12-Month)

Bank Statements (24-Month)

Primary Residence

Second Home

Investment Property

Purchase

Refinance

List item

+6 more

Bank Statement Program

A perfect fit for self-employed borrowers

Min. FICO 620 | Up to 90% LTV ○ Use personal, business, or combined bank statements ○ No tax returns required ○ Flexible income calculation options

Built for borrowers who need flexible documentation

Min. FICO 600 | Up to 80% LTV ○ Use a 1-year profit and loss statement to qualify ○ Eligible for SFRs, condos, and townhomes ○ Not available for first-time homebuyers

Min. FICO 660 | Up to 80% LTV ○ Only 1 year of self-employment required ○ Qualify using 12 months bank statements + prior W2/1099 ○ Must be in the same line of work

Flexible financing for borrowers outside traditional guidelines

Min. FICO 660 | Up to 85% LTV ○ Ideal for self-employed or asset-rich borrowers ○ Allows recent credit events like BK or foreclosure ○ Up to $3M loan amounts available

A full documentation option with expanded non-QM flexibility

No Score or Min. FICO 620 | Up to 80% CLTV ○ Loan amounts up to $4M ○ Flexible cash-in-hand limits based on CLTV ○ Built for borrowers who need non-agency options

A streamlined option for wage earners with stable employment

Min FICO 620 | Up to 80% LTV ○ No paystubs, W2s, tax returns, or 4506-C required ○ Uses completed FNMA Form 1005 ○ Requires 2-year history with the same employer

Close investment loans with fast, flexible qualification

Min. FICO 620 | Up to 80% LTV ○ Qualify using property cash flow (DSCR > 1.25) ○ No personal income or employment required ○ Short-term rentals allowed

Cash-flow based financing for investment properties

Min. FICO 620 | Up to 80% LTV ○ Qualify using rental income (DSCR-based) ○ No tax returns or employment needed ○ Options available for purchases and refinances

Built for experienced investors seeking higher loan amounts

Min. FICO 660 | Up to 70% LTV ○ Qualify using rental income (DSCR-based) ○ No personal income or employment required ○ Refinance and cash-out options available

Access U.S. financing without traditional domestic documentation

Min. FICO Not Required | Up to 75% LTV ○ Designed for non-U.S. citizens buying property in the U.S. ○ Flexible loan structures for international borrowers ○ Great for rental income or long-term appreciation

A full documentation option for international borrowers

Min FICO Not Required | Up to 75% LTV ○ Overseas assets can be used as reserves ○ One bank reference letter required ○ CPA letter for the last 2 years and year-to-date required

A full documentation option for international borrowers

Min FICO Not Required | Up to 75% LTV ○ Overseas assets can be used as reserves ○ One bank reference letter required ○ CPA letter for the last 2 years and year-to-date required

Min. FICO 620 | Up to 80% LTV ○ Convert liquid assets into qualifying income ○ No employment or income required ○ Ideal for retirees or high-net-worth clients

Min. FICO 640 | Loan Amounts Up to $1M ○ Flexible mortgage financing available for borrowers without a Social Security Number ○ Wage earners may qualify using WVOE and bank statements without W2s or paystubs ○ Available for purchase and refinance transactions across multiple occupancy types

Designed for borrowers outside traditional income guidelines

Min. FICO 660 | Up to 80% LTV ○ No DTI calculation required ○ No income or employment verification required ○ Available for primary, second homes, and investment properties

Designed for borrowers needing flexible income options

Min. FICO 700 | Up to 70% LTV ○ Use full doc, 1099, P&L, or bank statements ○ Asset utilization available for qualification ○ Ideal for self-employed and complex income borrowers

Min. FICO 660 | Up to 85% LTV ○ Flexible income documentation | 40-year options available ○ Use full doc, 1099, bank statements, or asset utilization ○ WVOE option available for simplified qualification

Min. FICO 660 | Up to 85% LTV ○ No income or employment verification required ○ Available for owner-occupied and second homes ○ Focus on credit profile and asset strength

Buy Your Next Home Before Selling Your Current One

Up to 75% LTV (70% in FL) | Loan Amounts Up to $2M ○ Leverage home equity to buy before you sell. ○ Available for primary, second homes, and investment properties. ○ Multiple income documentation options are available.

Qualify using assets instead of traditional income

Min. FICO 600 | Up to 80% LTV Purchase ○ Qualify using liquid assets with no traditional income verification required ○ Flexible qualification structure designed for cash-heavy borrowers ○ Available for primary residences and second homes with simplified underwriting

Lower monthly payments with flexible financing options

Min. FICO 640 | Loan Amounts Up to $3M ○ Interest-only payment options available with lower initial monthly payments ○ Available for primary residences, second homes, and investment properties ○ Flexible financing structure with 5-Year and 10-Year IO term options

Specialized Solutions for Unique Properties and Borrower Scenarios

Min. FICO 600 | Loan Amounts Up to $4M-$5M (Case-by-Case)

○ Financing available for specialty property types, including condotels, manufactured homes, short-term rentals, and 2-4 unit properties. ○ Multiple qualification options available, including DSCR, Bank Statements, Asset Utilization, WVOE, P&L, 1099, and Full Doc. ○ Flexible underwriting for borrowers with unique credit profiles, recent credit events, or non-traditional income sources.

Qualify Using Your Assets Instead of Employment Income

Min. FICO 620 | Loan Amounts Up to $4 Million

○ Qualify using eligible liquid assets instead of employment or self-employment income. ○ No tax returns, pay stubs, or employment verification required, and assets do not need to be liquidated. ○ Available for purchase and refinance transactions with financing up to 80% CLTV and DTI up to 55%.

A flexible mortgage solution for well-qualified borrowers

Min FICO 620 | Up to 97% LTV ○ Available for primary, second, and investment properties ○ No upfront funding fee required ○ Potentially lower rates for excellent credit

Min. FICO 620 | Up to 97% LTV ○ Eligible for primary, second, and investment properties ○ Uses after-completion appraised value ○ Can cover remodeling, repairs, ADUs, and more

Min. FICO 580 | As Low as 3.5% Down ○ Higher debt-to-income ratios allowed ○ Loans are assumable ○ Seller, builder, or lender credits may help with closing costs

Min. FICO 580 | 3.5% Down Payment ○ Available for purchase or refinance ○ Covers structural repairs, additions, HVAC, roofing, and more ○ Can also include new appliances

Min. FICO 580 | Up to 100% LTV ○ Finance purchase or refinance plus renovation costs in one VA loan ○ No down payment and no monthly mortgage insurance for eligible Veterans ○ Covers repairs, upgrades, and improvements based on after-completion value

Affordable financing for eligible rural and suburban homebuyers

Min. FICO 580 | 0% down ○ Available in eligible rural or suburban areas ○ Designed for qualifying households ○ Great option for low-down-payment buyers

Flexible financing solutions for high-value home purchases

Min. FICO 700 | Up to 90% LTV ○ Designed for high-balance and luxury properties ○ Competitive pricing with flexible loan structures ○ No PMI options available (20% down) ○ Ideal for primary, second homes, or investment properties

Financing for business growth and real estate investment

Min. FICO 680 | Up to 75% LTV ○ Access funds for expansion or commercial real estate ○ Potential tax advantages may apply ○ Built for investor and business-use scenarios

Fast and flexible financing outside traditional guidelines

No minimum FICO | Up to 70% LTV ○ Helpful for borrowers with poor credit ○ Often easier to qualify for than traditional loans ○ Built for speed and flexibility

Short-term financing for acquisition, renovation, and resale

Min. FICO 660 | 20% Down Required ○ Finance purchase price and rehab costs in one loan ○ No payments required for the first 12 months ○ Interest rates typically range from 9%–11%

Build your home with one loan, one approval, and one closing

Min FICO 700 | Up to 95% LTV ○One-time closing, no need to refinance after construction ○ Lock your rate upfront for long-term stability ○ Finance construction costs and land in one loan ○ Streamlined process from build to move-in

Fast funding for project-based real estate opportunities

No minimum FICO | Up to 82% LTC ○ 1% origination fee to Easy Street Capital ○ Built for quick execution ○ Ideal for construction-focused financing needs

Long-term financing for rental and investment properties

Min. FICO 660 | Up to 80% LTV ○ Eligible for single rentals, vacation homes, and multi-unit portfolios ○ Competitive rates available ○ Built for long-term real estate investors

Stand-alone second lien | Flexible property eligibility ○ Fixed-rate second mortgage structure ○ No need to refinance existing first lien ○ Ideal for leveraging equity while keeping low rates

Designed for homeowners looking to maximize financing

First + HELOC combo | Reduce out-of-pocket costs ○ Simultaneous financing with first lien and HELOC ○ Access additional funds at closing ○ Flexible structure for purchase transactions

Designed for homeowners needing fixed second lien financing

Up to 85% CLTV | Fixed-rate second lien ○ Predictable fixed monthly payments ○ Access equity without refinancing the first mortgage ○ Ideal for cash-out or consolidation

Designed for homeowners seeking stable equity access

Fixed-rate HELOC | Predictable payments ○ Based on CLTV and credit profile ○ Access funds without refinancing the first mortgage ○ Ideal for long-term planning and stability

Designed for homeowners needing additional financing

Fixed-term second lien | Access equity without refinance ○ Standard second mortgage structure ○ Allows gift funds in some cases ○ Ideal for cash-out or supplemental financing

Designed for homeowners looking to access their equity

Flexible condo eligibility | Primary, second, and investment use ○ Qualify using full doc or asset utilization ○ Available for owner-occupied and investment properties ○ Ideal for cash-out, debt consolidation, or investing

Financing for medical professionals at different career stages

Min. FICO 680 | Up to 95% LTV ○ Up to $2M for licensed professionals who completed residency ○ Up to $1M for residents, interns, and fellows ○ Primary residence purchase only

Extra lender credit support to reduce borrower costs

Min. FICO 640 | Up to 97% LTV ○ Credit comes from premium pricing ○ Can help reduce cash needed at closing ○ Useful for affordability-focused financing

Financing for condos that fall outside standard lending guidelines

Min. FICO 660 | Up to 85% LTV ○ Access financing for non-traditional condo properties ○ Ideal for projects that do not meet agency standards ○ Helps open more condo purchase opportunities

Flexible financing for a wide range of manufactured housing

FICO as Low as 500 | Up to 100% Financing on Select Programs ○ Available with FHA, VA, USDA, and Conventional options ○ Eligible for singlewide, doublewide, and triplewide homes ○ Includes purchase, rate-term, and cash-out options

Financing for borrowers without traditional credit

Min. FICO Not Required | Up to 97% LTV ○ Alternative credit like rent, utilities, and phone bills may be used ○ Available with FHA, FNMA, and VA options ○ Eligible for SFRs, condos, PUDs, and some manufactured homes

Access home equity through a reverse mortgage structure

Min. FICO 600 | Loan Amounts Starting at $40,000+ ○ Convert home equity into accessible funds with no monthly mortgage payments ○ Available for primary residence refinance with required counseling ○ Residual income and credit requirements apply based on borrower profile

Designed for very-low-income first-time homebuyers

Min FICO 620 | Up to 97% LTV ○ Helps eliminate upfront cash barriers ○ Includes an assistance component to offset costs ○ Ideal for borrowers with limited savings

Grant-based assistance | No repayment required ○ Available with FHA and conventional loans ○ Helps cover down payment and closing costs ○ Income-targeted eligibility, Ideal for first-time buyers

Perfect for first-time homebuyers with limited funds

FHA 580–599 FICO | No Min. LTV or Max. CLTV ○ Forgivable or repayable assistance options ○ Available with FHA and USDA loans ○ Helps cover down payment and closing costs

Designed for buyers needing flexible assistance options

Min. FICO 620 | Up to 97% LTV ○ First-time homebuyer eligibility may not be required ○ Helps reduce upfront cash needed ○ Flexible qualification structure

Down payment assistance with shared appreciation ○ Second lien tied to future home value ○ Reduces initial cash investment ○ Ideal for long-term homeowners

Min. FICO 620 | Up to 97% LTV ○ Available for standard and blended credit profiles ○ Helps reduce cash to close ○ Works with FHA financing ○ Supports first-time homebuyers

Designed for eligible Florida homebuyers and occupations

Min. FICO 640 | Up to 97% LTV ○ State-specific program with income/occupation eligibility ○ Helps cover down payment and closing costs ○ Supports workforce housing initiatives ○ Ideal for primary residence purchases

Min. FICO 620 | Up to 97% LTV ○ Allows seller concession flexibility ○ DU approve/eligible required ○ Helps reduce upfront costs ○ Works with standard agency financing

Min. FICO 620 | Up to 97% LTV ○ Available for standard and blended credit profiles ○ Helps reduce cash to close ○ Works with FHA financing ○ Supports first-time homebuyers

Financing Solutions for Hotel-Style Condominium Properties

Min. FICO 600 | Loan Amounts Up to $4M ○ Finance eligible condotel and resort-style properties with flexible qualification options. ○ Full Doc, Bank Statement, and DSCR programs available for owner-occupied, second home, and investment properties. ○ Up to 75% LTV purchases, Airbnb income eligibility, entity vesting options, and no reserve requirements.

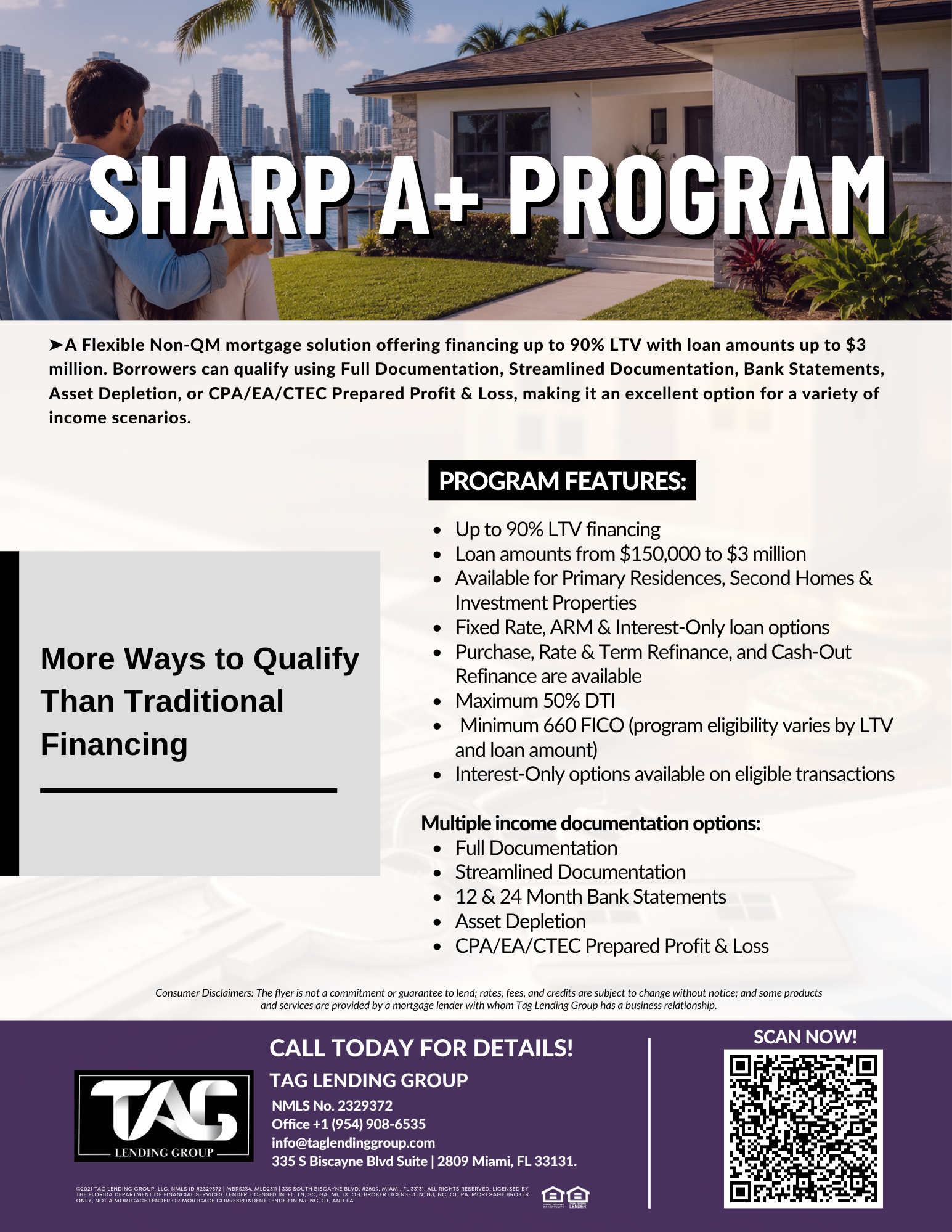

Expanded Non-QM Financing with Multiple Ways to Qualify

Min. FICO 660 | Up to 90% LTV | Loan Amounts from $150K to $3M

○ Multiple income documentation options available. ○ Available for primary, second home, and investment properties. ○ Purchase, rate-term, and cash-out refinance options.

Access Your Home Equity Without Refinancing Your First Mortgage

Min. FICO 620 | Up to 89% CLTV | Credit Lines from $5K to $1M ○ Access your home's available equity. ○ Fixed-rate initial draw with additional draw options. ○ Available for owner-occupied and investment properties.

To edit a card, just replace the image URL and the two button links inside that card block. You can also duplicate any card and change the title and badge text.

What are Loan Options?

Once you think through your goals and determine how much home your budget can handle, it’s time to choose a mortgage. With so many different mortgages available, choosing one may seem overwhelming. The good news is that when you work with Tag Lending Group. Our AI Mortgage Solution System will walk you through every step of the way!

.png)

%20(1).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

-1.png)

.png)

.png)

.png)

.png?width=150&height=75&name=Union%20Home%20Mortgagte%20(TPO).png)

.png?width=150&height=75&name=Union%20Home%20Mortgagte%20(SPM).png)

.png?width=150&height=75&name=TLS%20(the%20Loan%20Store).png)

).png?)

).png?width=2000&height=1414&name=TAG%20LENDING%20GROUP%20LOAN%20PROGRAMS%20LIBRARY%202026%20(A4%20(Landscape)).png "TAG LENDING GROUP LOAN PROGRAMS LIBRARY 2026 (A4 (Landscape))")