Self-employed buyers are not rare anymore. They are business owners, consultants, contractors, creators, and 1099 earners who often earn strong income but show very little on paper after deductions. Too often, solid purchase contracts fall apart because traditional underwriting relies heavily on tax returns.

However, there is a more strategic solution.

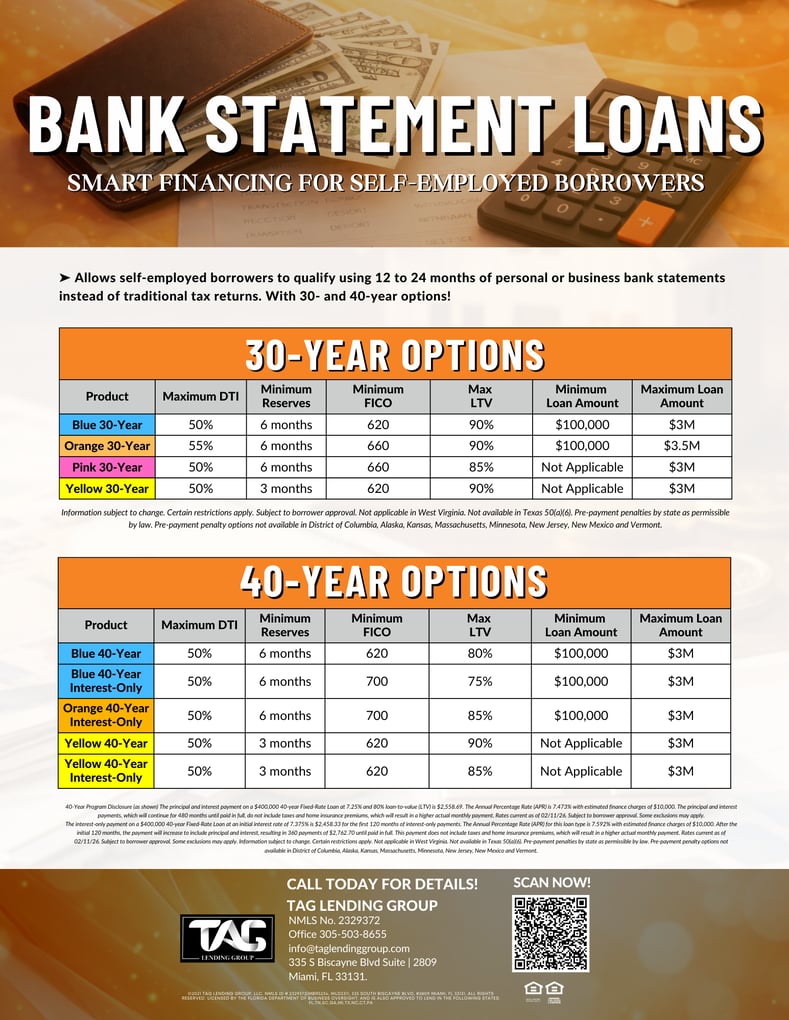

40-year bank statement loans, along with traditional 30-year options, allow qualified borrowers to use 12 to 24 months of bank statements to document income instead of tax returns. As a result, Realtors can keep more deals alive, serve a growing segment of the market, and offer real financing solutions when others cannot.

When Tax Returns Don’t Tell the Full Story

Many self-employed borrowers look strong financially. Deposits are consistent. Cash flow is healthy. Liquidity is available. Yet tax returns often reflect aggressive deductions that reduce net income below conventional qualifying thresholds.

That does not mean the borrower cannot afford the home. It simply means the income needs to be calculated differently.

Bank statement loans focus on verified deposits over a 12- to 24-month period. Instead of relying on Schedule C net income, lenders analyze actual cash flow patterns. This approach creates qualification opportunities that traditional underwriting may overlook.

For Realtors, this means:

- Fewer deals lost due to tax write-offs

- Stronger retention of self-employed buyers

- Expanded financing conversations during pre-approval

- Increased credibility when navigating complex income scenarios

In today’s market, understanding this option is not optional. It is a competitive advantage.

The 40-Year Structure: A Strategic Affordability Tool

While the program offers both 30-year and 40-year terms, the 40-year option introduces meaningful flexibility. By extending the amortization period, monthly principal and interest payments are reduced. Consequently, buyers may improve their debt-to-income ratios and expand purchasing power.

Additionally, certain 40-year structures offer interest-only options for qualified borrowers. This can significantly lower the initial payment, providing enhanced cash flow management for entrepreneurs with variable income cycles.

The 30-year option remains a strong and traditional choice for long-term equity growth. However, having both structures available allows buyers to align financing with their broader financial strategy.

Key highlights include:

- 30-year and 40-year term options

- Interest-only availability on select 40-year programs

- Debt-to-income ratios up to 55%

- Loan-to-value ratios up to 90% on certain products

- Loan amounts up to $3.5 million

For Realtors, this flexibility often prevents renegotiation. Instead of reducing the price to fit a payment, you can explore structural adjustments that preserve the transaction.

A Stronger Referral and Retention Strategy

Realtors who understand flexible financing solutions position themselves differently in the marketplace. When you can confidently discuss 30- and 40-year bank statement options, you elevate your role from facilitator to strategic advisor.

Self-employed buyers frequently operate within networks of other business owners. A smooth transaction often leads to referrals within that professional circle. Moreover, CPAs and financial advisors value partners who understand alternative income documentation solutions.

This strengthens your business by:

- Expanding your referral base among entrepreneurs

- Increasing closing consistency

- Reducing deal fallout from income documentation issues

- Enhancing your professional reputation

Bank statement loans are not a workaround. They are a structured financing solution built around modern income realities.

Final Thoughts

With both 30- and 40-year options available, bank statement loans provide a legitimate and scalable path to homeownership for self-employed buyers. Flexible income documentation, competitive LTV allowances, DTIs up to 55%, and loan limits up to $3.5 million create meaningful opportunity.

The next time a self-employed client appears challenging on paper, pause before assuming the deal is lost. The solution may not require a different buyer. It may simply require the right loan structure.

Download Our Bank Statement Loans Cheat Sheet!

.png?width=262&height=339&name=Christina%20mosquera%20Loan%20Programs%20(1%25%20Giveback).png)

%20(1).png?width=262&height=339&name=Christina%20mosquera%20Loan%20Programs%20(1%25%20Giveback)%20(1).png)

Unlocking Real Estate Success:

Tag Lending Group's Client Funnel Retention Program

In this dynamic video, we break down the essential components of our intake form and showcase how it empowers you to understand your return on investment, lead sources, and client demographics. Discover how we harness this data to fine-tune your marketing strategy and drive impressive results.🏠🔑

.png?width=500&height=647&name=TLG%20FLYERS%20(4).png)