In today’s market, affordability isn’t just a concern, it’s the conversation. That’s exactly where Freddie Mac HomeOne steps in and delivers. This program is designed to help first-time homebuyers move from “thinking about it” to “keys in hand” with fewer barriers and more flexibility.

Unlike many traditional loan options, HomeOne removes geographic and income restrictions, which immediately expands your pool of eligible buyers. That means more opportunities to convert leads into closings. Additionally, with as little as 3% down and up to 97% LTV, buyers who once felt sidelined can now realistically compete in the market.

From a real estate professional’s perspective, this isn’t just another loan program, it’s a tool to create momentum. More qualified buyers means more offers, faster transactions, and ultimately, more deals getting across the finish line.

Built for Today’s Buyer: Flexible Guidelines That Actually Work

Let’s be real, rigid guidelines kill deals. HomeOne takes a different approach by leaning into flexibility while still maintaining agency backing. That balance is where the magic happens.

First, credit is evaluated based on AUS findings, not arbitrary overlays. This allows more buyers to qualify without unnecessary friction. In addition, gift funds are permitted, which is a huge win for first-time buyers who often rely on family support to bridge the gap.

Here’s where the program really shines:

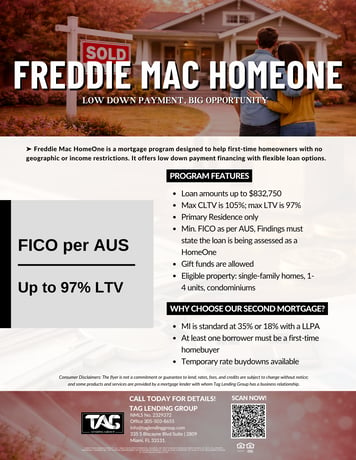

- Loan amounts up to $832,750

- Maximum LTV of 97%

- CLTV up to 105%

- Minimum FICO determined by AUS

- Primary residence only

- Eligible properties include single-family homes, 1–4 units, and condominiums

Because of this structure, agents can confidently work with a wider range of clients, including those who may have been told “not yet” by other lenders. Now, it becomes “let’s structure it right.”

Turning Hesitation into Action: Why Buyers Say Yes

Every buyer hesitates at some point, usually around money. Down payment, monthly payment, or just fear of overextending. HomeOne directly addresses those concerns and gives agents a stronger value proposition during conversations.

The low down payment requirement is the obvious headline, but the real leverage comes from how the program positions affordability overall. With options like temporary rate buydowns, you can create a smoother entry point for buyers navigating today’s rate environment.

Also worth noting:

- Mortgage insurance options are standard, with flexibility at 35% or 18% coverage depending on LLPA structure

- At least one borrower must be a first-time homebuyer, which aligns perfectly with the largest active buyer segment today

So instead of pushing buyers, you’re guiding them. That shift in approach builds trust and speeds up decision-making.

Your Competitive Edge: How Agents Win More Deals with HomeOne

In a competitive market, the agents who win are the ones who bring solutions, not just showings. HomeOne gives you that edge.

Think about it this way, when inventory is tight and affordability is stretched, buyers need more than listings. They need strategy. By introducing a program like HomeOne early in the conversation, you position yourself as a resource, not just a salesperson.

Even better, this program pairs perfectly with proactive outreach. Whether you’re working your pipeline, nurturing renters, or engaging online leads, having a clear, simple message like “3% down, conventional financing” cuts through the noise instantly.

And let’s not ignore the partnership angle. When lenders and agents align around programs like this, deals move cleaner, faster, and with fewer surprises. That’s how you build a repeatable system, not just one-off closings.

Final Take: More Than a Loan, It’s a Deal-Creating Tool

Freddie Mac HomeOne isn’t just another product on a rate sheet. It’s a strategic advantage for both agents and buyers. It removes common roadblocks, expands eligibility, and creates real opportunities in a market where every edge matters.

For real estate professionals, the takeaway is simple. If you’re not actively using programs like HomeOne in your conversations, you’re leaving deals on the table. On the flip side, when you do leverage it correctly, you turn uncertainty into action and prospects into homeowners.

And at the end of the day, that’s the whole game.

Download Our Cheat Sheet!

.png?width=262&height=339&name=Christina%20mosquera%20Loan%20Programs%20(1%25%20Giveback).png)

%20(1).png?width=262&height=339&name=Christina%20mosquera%20Loan%20Programs%20(1%25%20Giveback)%20(1).png)

Unlocking Real Estate Success:

Tag Lending Group's Client Funnel Retention Program

In this dynamic video, we break down the essential components of our intake form and showcase how it empowers you to understand your return on investment, lead sources, and client demographics. Discover how we harness this data to fine-tune your marketing strategy and drive impressive results.🏠🔑

.png?width=500&height=647&name=TLG%20FLYERS%20(4).png)